2025 Q2 Global Economic Outlook (II) - Japan, Europe, and the United Kingdom

In the first quarter of 2025, the global economy has seen a brief period of stabilization, supported by easing inflation and growing expectations of policy shifts. However, the upcoming announcement of new U.S. tariffs has become a key focus for global markets, posing increased external pressure on export-driven economies. Last week, we discussed the economic outlook for the United States and China—this week, our focus turns to Japan, Europe, and the United Kingdom.

Japan

Japan’s economy demonstrated a degree of resilience in the first quarter of 2025, supported by recovering consumption and tourism. However, deeper structural challenges are beginning to surface—most notably in two areas: deteriorating external trade prospects and the reacceleration of domestic inflation.

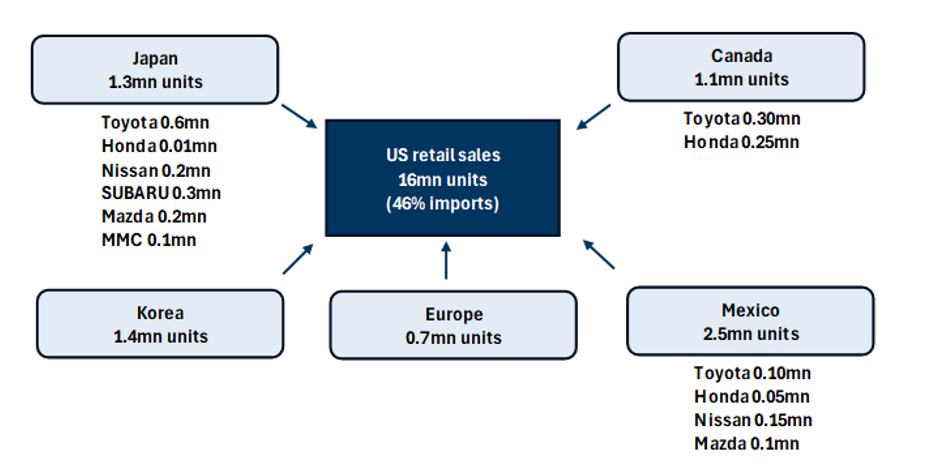

Japan’s export structure is highly concentrated, particularly toward the United States. Automobiles and auto parts account for more than 30% of Japan’s total exports to the U.S. As the U.S. administration considers raising tariffs on so-called “critical imports,” Japan’s automotive supply chain has become one of the most exposed sectors. According to Goldman Sachs’ baseline scenario, a 25-percentage point across-the-board tariff on imported autos would drag Japan’s GDP down by about 0.1 percentage points. If the tariff were imposed on Japan alone, the economic hit could expand to 0.4 percentage points. Such an external shock would directly suppress manufacturing profitability and export momentum, increasing Japan’s reliance on domestic demand to sustain growth.

At the same time, inflation has not improved as much as headline data might suggest. While core CPI in February edged down slightly to 2.1%, high-frequency and structural indicators point to widespread price pressures—particularly in services and food. The recent moderation in inflation likely reflects temporary government subsidies and base effects, rather than a durable trend.

More importantly, the annual Shunto (spring wage negotiations) is ushering in a new wave of wage increases that will likely push inflation structurally higher. Major manufacturers have already committed to wage hikes exceeding 4% - a level not seen in two decades. Early signs of a wage-price spiral are emerging, and price stickiness in the services sector is intensifying. This represents a structural break from Japan’s long-standing low-inflation regime.

In this environment, the Bank of Japan’s policy options are becoming increasingly constrained. Market consensus previously assumed that the BOJ would keep interest rates unchanged through mid-2025 and continue stabilizing markets via asset purchases. However, the current environment has clearly shifted. On one hand, persistent inflation pressure and rising wages are eroding the justification for zero interest rates. On the other, asymmetric trade shocks from U.S. tariffs could force the BOJ into a stagflation-like tightening cycle, despite lackluster external demand. Although the yen has remained relatively stable in recent months, we see a reassessment of Japanese asset risks by global investors which will revive depreciation pressure.

Given this backdrop, a rate hike is becoming almost unavoidable. The BOJ will be forced to further tighten policy in response to both external shocks and domestic inflation dynamics.

Euro Area

In the first quarter of 2025, Europe unexpectedly emerged as a relative outperformer in global markets. Amid rising U.S. political and trade uncertainty, investors have re-evaluated Europe’s perceived stability, viewing it as a “strategic safe zone.” Inflation in the euro area continues to fall, which has fueled expectations that the ECB could be among the first major central banks to start easing. At the same time, Germany’s fiscal policy shift and enhanced EU-level budget coordination have improved the growth outlook in Central and Eastern Europe, boosting the appeal of European bonds and FX assets.

However, the foundations of this safe-haven logic are far from secure. Structural fragmentation remains a significant vulnerability across the eurozone. Germany, traditionally the region’s growth engine, is now stagnating. Its manufacturing PMI has been in contraction for five consecutive months through the end of 2024, and business investment sentiment remains subdued.

Meanwhile, countries like France, Italy, and Spain have implemented fiscal stimulus measures, but the overall growth impulse has been modest. In Central and Eastern Europe—countries such as Poland and Czechia—currency appreciation has helped cool inflation more quickly, and we anticipate that rate cuts will begin in Q2 2025.

Investor optimism in Europe is primarily driven by political symbolism, namely NATO and EU leaders reiterating their commitment to “protect the interests of allies.” These statements have been rapidly priced into defense stocks and sovereign bonds. However, it’s crucial to note that the U.S. has not yet officially imposed tariffs on Europe (until April 2nd, we shall see) — but this is just a matter of time. Should the U.S. cite “industrial security,” “digital services taxation,” or “automotive components” as justification for tariffs, European markets could face a systemic shock, unraveling the current “safe haven” narrative.

Additionally, Germany and France are classified as high-risk countries under the U.S. “Dirty 15” list. If tariffs or sanctions are implemented, Europe’s manufacturing sector would face a double blow: falling external demand and internal fiscal reallocation toward defense and immigration management, squeezing funding for green energy and digital transformation.

In short, while Europe has attracted capital inflows in early 2025, its structural growth challenges, dependence on U.S. trade, and internal coordination difficulties have not disappeared. The euro’s recent strength is less of a reflection of improved fundamentals and more a mirror image of USD weakness.

United Kingdom

The UK remains stuck in a classic stagflationary pattern in Q1 2025—characterized by low growth and high inflation. GDP is expected to grow by just 0.4%, below the post-COVID average. Consumer spending remains weak, held down by elevated interest rates and high living costs. While the housing market has shown some technical stabilization, a sustained rebound has yet to materialize.

Though inflation has come down from last year’s peak, CPI remains above 2.8%, and price pressures in services remain elevated. The Bank of England has held interest rates steady at 4.5%, but we expect the first rate cut to follow the May or June general election. That said, the path of monetary policy is highly dependent on political outcomes. The ruling and opposition parties have sharply differing views on fiscal discipline, tax reform, and the UK’s post-Brexit trade positioning—making it difficult for markets to form a clear forward-looking policy view.

Externally, the UK is not immune to potential U.S. or EU tariff escalations. While the UK is no longer part of the EU, its industrial structure is highly similar—particularly in autos, machinery, and medical devices. These exports could easily be swept into broader “critical import” categories. If U.S. tariffs are expanded to cover European goods, UK products may suffer collateral damage. Moreover, post-Brexit, the UK lacks a fiscal or monetary union, leaving it without coordinated policy tools to absorb external shocks. As a result, the Bank of England is increasingly the sole line of defense—putting pressure on markets and increasing financial fragility.

Conclusion:

The global economic landscape in Q1 2025 is not one of “broad-based recovery,” but rather one of reallocated risk and constrained policy space. Markets are now re-evaluating the geographic distribution of risk, the actual limits of monetary and fiscal flexibility, and how central banks will navigate the inflation-growth tradeoff.

Japan is being pushed into a reluctant tightening cycle. The Eurozone is caught in a fiscal-political tug-of-war. The UK remains mired in stagnation and politicized policymaking. And hanging over all of them is the not-yet-triggered U.S. tariff threat—a policy ax suspended above the world’s major exporting economies. Should it fall, it will upend today’s fragile balance.